The Game's Greatest Strategy

Summary: The invention of the iPhone and cloud computing were “Twin Big Bangs” that fully unlocked the potential of the internet to reshape The Game of Capitalism. Thirty companies that run on software coalesced around these technologies. They re-engineered the basis of competition in several of the biggest consumer discretionary end markets. They reshaped enterprise technology budgets. Collectively, their value creation amounted to $24T through the end of 2025 – nearly half of total value creation in the S&P 500.

The business models that emerged from the Twin Big Bangs ushered in a new phase of maximalist capitalism that reshaped modern life. They brought obvious first order benefits: more choice, convenience, and opportunity to get rich. But they also introduced potential negative second order effects: crowding out, envy, and agency erosion. The maximalist strategies of consumer internet companies are engineered for overuse – and so risk having the negative second order effects subsume the positive first order effects.

For individuals, winning in The Game requires awareness of how the mobile internet reshaped it. Without this we risk missing the negative second order effects of overuse. We risk becoming marionettes – overly responsive to the algorithmic strings of the consumer internet.

Part 1: Big Bang Bookends – From the iPhone to the LLM

Whether you are driving change or getting blindsided by it, you rarely see it coming – when a “big thing” begins and ends. King George III did not realize he had a pending war for his most valuable colony when he got news in January 1774 that Bostonians dressed as Indians dumped 200 tons of tea into the Boston Harbor. The “Indians” that night had a better sense but could not fathom the history unfolding either.

Steve Ballmer famously laughed off the iPhone when Steve Jobs unveiled it in early 2007. Even Jobs did not grasp how big it would become – he set the goal to grab 1% share of the phone market – about ten million units – by 2008 and “go from there.”[1]

Looking back, we see the big inflection points more clearly. The late 1990s internet boom was not wrong – just early. The infrastructure to operate the optimists’ vision wasn’t ready yet. The mobile and cloud computing era began when that infrastructure finally arrived: two “big bangs” three months apart. The first iPhone shipped in June 2007. Amazon Web Services (“AWS”) launched its Elastic Cloud Compute (“EC2”) in October 2007.

Most of how the internet re-shaped The Game of Capitalism (and life beyond the game) in the twenty first century flowed from those product launches. They brought us the internet in our pockets and the computing infrastructure to support the explosive growth of mobile apps that the iPhone spawned. Those dual pieces of infrastructure were the skeleton keys that unlocked the internet’s doors of potential.

The impact of the iPhone is obvious: 91% of U.S. adults own smartphones (56% are iPhones). The average iPhone user spends 5 hours a day on their device.

The impact of AWS’s EC2 hidden to most consumers but just as essential. It made computing elastic – with EC2, companies could scale up instantly without building their own infrastructure. This collapsed investment timelines from years to minutes. Instagram, Snap, Pinterest, Airbnb, Spotify, Uber, DoorDash, Coinbase, and Stripe all scaled on AWS. These firms could grow their user bases and test features without first raising billions to build data centers to support uncertain future demand.

Revenues from players than run the mobile internet and cloud computing software ecosystem are still growing in the high teens (5-10x faster than GDP). They still underpin our digital lives.

But we may look back and conclude that their era as “the big thing” ended when ChatGPT launched on November 30 2022. That’s what the stock market is hinting at: from June 2007 to November 2022, Apple’s stock rose 32x and Amazon’s 27x (versus the S&P 500’s 2.6x). Since ChatGPT launched, Apple is up ~80% and Amazon ~125% (vs. the S&P 500 up 70%). Amazon’s stock is flat since mid-2024. Both companies still trade at premium valuations; investors see them as future winners. But their outperformance spread has narrowed. And they are no longer priced as the dominant power law winners they once were.

Throughout this project, I use “tech” to refer to the IT ecosystem: software and the infrastructure (like mobile phones and cloud computing data center) that powers it. This isn’t a perfect definition; it’s not exhaustive of all tech advancement. But it captures most of the wealth created in public markets through technology since 2007.

Collectively, the key players in this ecosystem reshaped The Game of Capitalism. They forged the greatest strategies the game has ever seen. They do not operate as a unit; different players within have different strategies. Throughout, I call out and explore impacts tied to specific subsets or players of this tech complex (like social media, or gig economy apps).

Part 2: The Birth of The Software Cerberus

“Every once in a while, a revolutionary product comes along that changes everything… today, we’re introducing three… a widescreen iPod with touch controls, a revolutionary mobile phone, and a breakthrough internet communications device.” ~ Steve Jobs, 7 January 2007

For all his swagger at the iPhone launch, even Jobs missed how the iPhone would reshape the chessboard of the tech industry. He saw his new product as revolutionary for consumers, not as the new center of gravity for value creation that it would become.

During the iPhone launch presentation Jobs suggested “the [iPhone’s] killer app [would be] making calls.” His ideas about the iPhone as an internet device were surprisingly utilitarian: email, GPS, web surfing. After the iPhone’s early success Jobs resisted his own executive team and Board when they pushed to open the App Store to third-party apps.

Today Apple is the main toll road operator of the digital economy. It collects a 30% fee on subscriptions purchased through the app store. It intermediates what data digital advertisers can collect on their iPhone app users. The birth of the “platform economy” – with Apple as its center of gravity – happened almost by accident.

The audience did not sense the future either. They cheered the new widescreen iPod announcement. But when Jobs introduced the “breakthrough internet communications device,” they responded with tepid bemusement. They did not get it yet.

Apple’s featured partner at the iPhone launch was Google. When Jobs finished, he handed the mic to Google CEO (and Apple Board Director) Eric Schmidt. Ironically, Schmidt seemed to intuit the shifting center of gravity more than Jobs. He joked about merging into “AppleGoo” and observed that the architecture of the internet allowed the two companies to “merge without merging.” Today Google pays Apple ~$20B per year to be the default search engine on Apple devices. Apple still has never made a serious effort to build its own search engine.

Schmidt spoke about the Google Maps on the iPhone as being “the first of a whole new generation of data services” running on “powerful cloud-based computers, Google being – we hope – a leading representative.” More than anyone else on stage, he seemed to foresee the explosive mobile internet growth ahead. Google Cloud Platform (GCP) was launched fourteen months later, in April 2008. It let third party developers to build web applications on the same infrastructure that Google used for Search, Gmail and other products.

Amazon beat Google to market in cloud computing.[1] When they released EC2 in October 2007, AWS had a modest $20M business renting out storage and infrastructure to nascent internet businesses like Netflix on a pay-as-you-go model. Compared to the iPhone, EC2 launched quietly – just a press release announcing “Amazon EC2: Now in Unlimited Beta and Launching New Instance Types.”[2]

The tech world didn’t realize it at the time, but Amazon had just dropped the operating system blueprint for scaling on the internet. Young companies could buy servers, storage applications from AWS without building their own data centers. Several of today’s largest internet companies – including Airbnb, DoorDash, and Pinterest – were built off AWS from Day 1. They never owned a data center. Industry analysts estimated that AWS hit $500M of sales by 2010. When Amazon first disclosed AWS revenue in 2014 it had reached $4.6B. By 2025, AWS was generating $120B in revenue and more than $40B in operating profit; 50-60% of Amazon’s total profit.

Jobs’ resistance to opening up the App Store did not last long. Within months of the iPhone release, hackers found workarounds to let users to jailbreak their phones and install custom third party apps – games, custom ringtones and other simple stuff. Apple’s development team worked built a more secure “software developer kit” (SDK). By October Jobs relented: Apple announced that they would release an SDK in early 2008. The app store opened to third party apps in July 2008 with an initial library of 500 apps.

By August, Jobs admitted that the app store had surpassed all expectations. So he revised his strategy - Apple leaned in. In January 2009, the company launched its famous “there’s an app for that” ad campaign, shifting the marketing focus for the iPhone from its hardware device features to its software platform versatility. The phrase entered the U.S. culture and lexicon – shorthand for the idea that mobile software could address and solve any problem of modern life. Apple applied for a trademark for the phrase by the end of the year. As of 2025, Apple’s services division (largely app store fees) generates $27B in profit, about ~25% of Apple’s total.

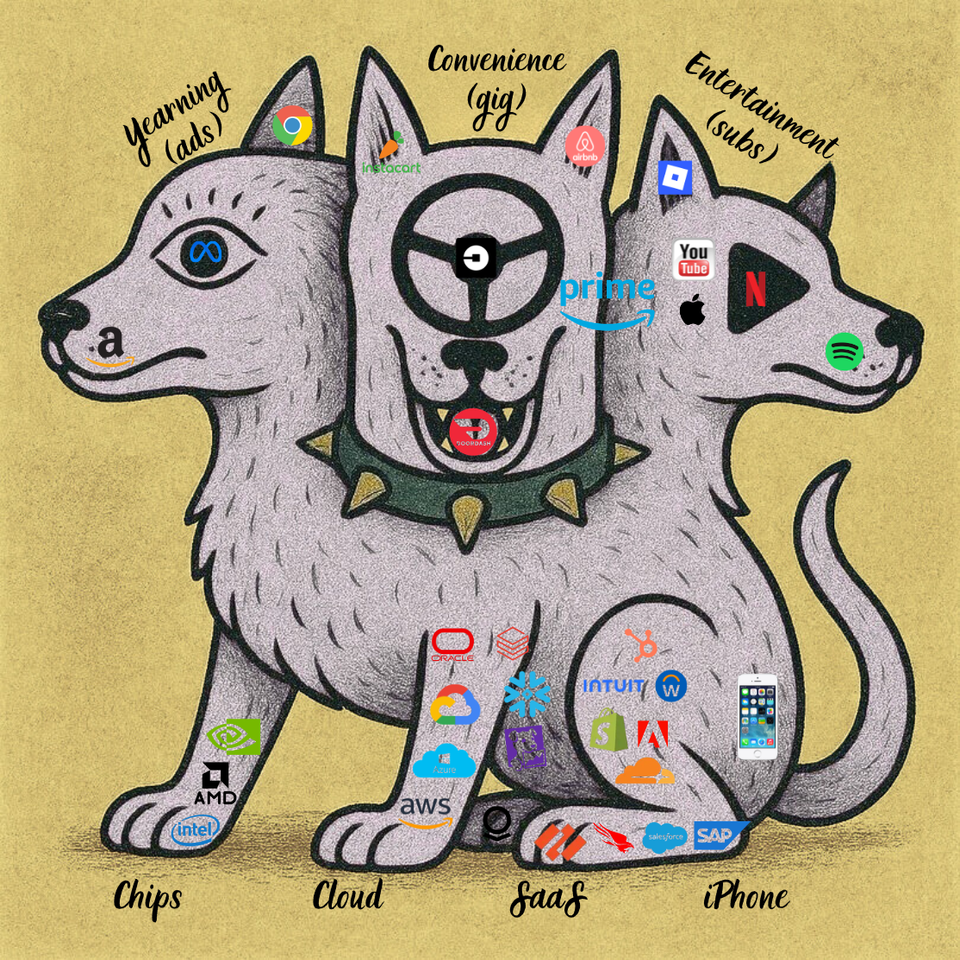

With hindsight, the endgame ecosystem structure of the cloud/mobile era was already emergent from Twin Big Bangs. Apple became the toll collector of the mobile consumer internet alongside Google. In quiet co-opetition, these two monetized end consumers through online ads and media subscriptions. Amazon was the first “gig economy” player – it used software to expand consumer product choice and to engineer the store trip out of the purchase process.

Using the software it had built to run its retail business, Amazon staked claim as the “picks and shovels” seller to emergent internet upstarts – providing them the computing infrastructure to scale. Microsoft and Google succeeded as fast followers. Intel, AMD and (increasingly) Nvidia sold the chips into the data centers that power the internet’s infrastructure. Together, these gatekeepers enabled the writing, distribution, and consumer adoption of software at unprecedented speed and scale.

Around these gatekeepers, new software transformed entire consumer end markets: movies and TV, music, video games, travel, restaurants, and taxis. New enterprise software had to be built to smoothly run the new cloud infrastructure. CrowdStrike and Palo Alto Networks manage security. Palantir, Databricks, Snowflake and MongoDB help to structure, unify and analyze data across the network to improve business decisions. Datadog provides continuous monitoring of all apps running in the cloud. Of the pure enterprise power players, only Palantir existed before the iPhone. The rest of these software companies were not even founded before its launch.

What gave forth was The Software Cerberus – a collection of thirty companies hoovering up revenues across seven distinct revenue streams. It devours consumer wallet share through digital ads, digital networks of gig contractors, and media subscriptions. It hoovers up enterprise spending through software licenses and computing power. Phones anchor the consumer spending; microchips anchor enterprise spending.

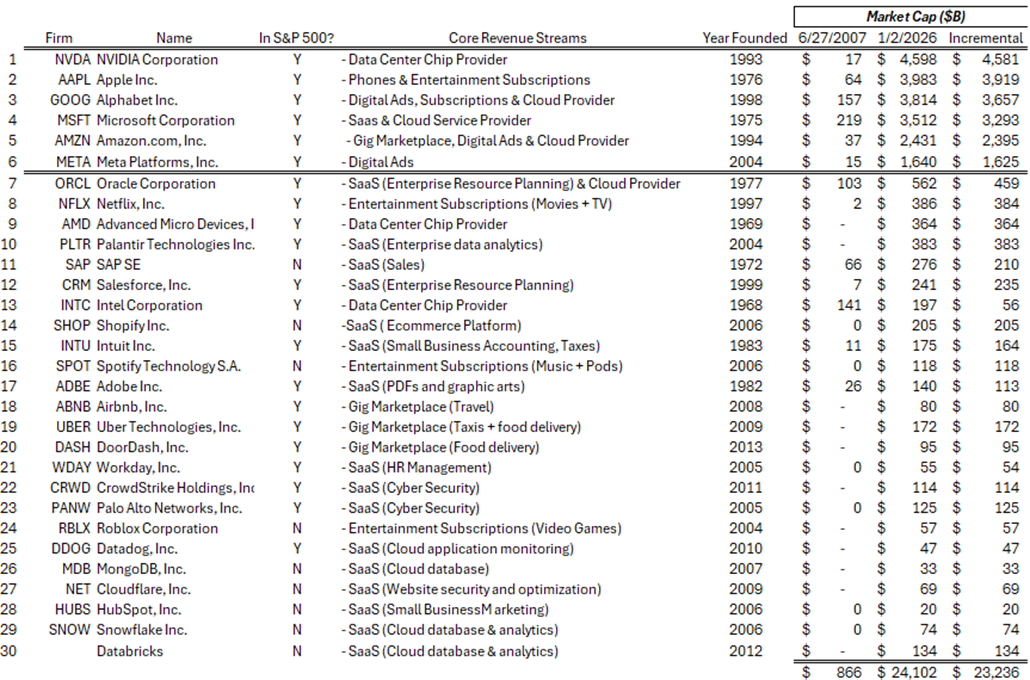

Together the 30 companies inside the Cerberus created $24 trillion in value from the iPhone launch through the end of 2025. That’s about 50% of all the value created in the S&P 500 during the same period.

Part 3: What The Game Delivered – The Abundance Dividend and Its Squandering

The Cerberus is dominating the game with an abundance dividend – more choice, more convenience, more time, more information access, and more job opportunity. Sure, the dividend has not been evenly distributed. But it reached everyone. More, more, more – that’s the motif and the mantra. The ecosystem is wildly and aggressively inclusionary by design.

Collectively, we’ve blown it. We’ve squandered the dividend.

How we reinvest our tech dividend is not just about how much we got. It’s a choice. We blow it because we don’t understand the trade-offs of tech usage, don’t have a game strategy, and lack execution discipline in daily life.

But the squandering is also an engineered outcome. The continued economic dominance of the consumer internet and the cloud is contingent on us mindlessly reinvesting that abundance dividend back into its profit centers. There is no built-in mechanism to recognize when you’ve reached satiation or “diminishing marginal returns.” It is an all-you-can eat buffet – except one where restaurant profits go up, not down, as the guests eat more. This is not an excuse for us. It is just the reality of the game design.

The silver lining: there is plenty of fertile landscape for individuals and families to thrive and win aside The Cerberus. You don’t need to be a tech mogul or coding master.

Thriving requires four things. First, you must understand the game. How the economic incentives of tech companies shape product design and the outcomes those products are meant to engineer. Second, you must develop a plan to engage with the products to serve your ends, not those of the company. Third, you must own your attention and execute your plan with intention. Fourth, you must think across your inner economic personas – you must see beyond the whims of your inner consumer.

With an owner’s mindset and discipline, tech can help you get ahead – not just strip mine your attention span.

Part 4: The Beast’s Footprints - How Tech Rewired Modern Life

$24 trillion of new wealth creation is staggering, but it’s just a number. The real story sits behind the number: the large-scale re-shaping of our lived experience.

How do we spend our time? Our money? Who do we date? What do we know? How do we yearn? Where do we work?

The mobile internet seems superficially decoupled from real life – a digital world in bits, apart from our real world of atoms. But it is a portal into the real world. That is the means by which it reshapes the answers to these questions that mark out our lives.

The average American spends 5.25 hours per day on a smartphone – a sevenfold increase from fifteen years ago.[1] The average Gen Z spends over six hours.[2] U.S. e-commerce sales have increased fivefold as a percentage of total retail sales from mid-2007.[3] 50-60% of American couples today meet online; fewer than 20% did in 2007.[4] Online advertising went from $15 of every $100 spent in 2007 to nearly $80 in 2025.

Six themes emerge in the story of tech’s rewiring of modern life. Each follows a push-pull pattern: tech delivers an obvious first-order benefit (the dividend). But it also introduces a hidden second-order cost that can erode or overtake the benefit if left unchecked (the squandering). The game is designed to engineer squandering.

[The Economization of Life: From Choice Proliferation to Crowding Out]

Abundance of consumer choice is the clearest benefit of this era’s technology. It’s so obvious that it’s almost been forgotten. Choice ubiquity has redefined how we shop (Amazon vs. department stores), listen to music (Spotify vs. Tower Records), get news (podcasts vs. cable), order food (DoorDash vs. Domino’s) and manage our health (wellness apps vs. doctor visits).

On its face, more choice is an unambiguous good that we take for granted. With more good options, we tend to buy more.

“The essence of strategy is choosing what not to do” – Michael Porter

But all this digital choice crowds out other activities. It bombards our calendars and attention with a continuous flow of opportunities to transact. If you spend a third of your waking hours on a phone (as Gen Z does) you have less time for everything that you don’t do on a screen.

What you do becomes who you are. What you do less of defines you less. And what you don’t do at all ultimately disappears from your identity. We are spending much less time on activities that have grounded humans for generations: reading, praying, or spending unstructured time in person with friends.

There is another in-category crowding out effect in markets with finite supply – like the dating market. The swiping game generates new economic transactions out of a previously non-economic domain (finding a date and life partner). But it also leaves some people out of the dating game entirely. When everyone can see endless date options and winds up chasing the same “top” partners, they reject people who might have been their best match in a smaller pool. The result: more incels, more players, fewer lasting relationships. Dating participation has steadily declined during the mobile era—clear evidence of crowding out.

[Mimetic Yearning: From winner-take-all to envy]

The twin big bangs ushered in the greatest phase of new wealth creation in America in over a century. Record fortunes were made at the individual and company levels. Debate about wealth concentration is as old as the industrial age. We rarely achieve breakthrough innovation that raises material living standards without producing concentrated wealth. Inequality is a byproduct of creative destruction. This tension predates the mobile/cloud era and can’t be solved.

But mobile/cloud tech has magnified both the superstar effect and inequality, tightening the tension between them. Software development has been the core skill underpinning 21st-century technological progress. It has also been an unprecedented wealth-compounding lever for the bright, hungry, and resilient. The Forbes 400 shows this clearly: tech titans’ cumulative share of wealth rose from 23% in 1996 to 31% in 2007 to 66% in 2025.

Tech titans in the Forbes 400 held $2.5 trillion in 2025—up 56x from 1996 and 13x from 2007. Non-tech titans’ wealth grew only 9x and 3x over the same periods.[5] The superstar effect is far more pronounced in information technology than anywhere else. It is fractal – the same pattern appears at the individual and company levels. In mid-2007, tech companies made up 18-19% of the S&P 500’s market cap. [6] By 2025, that share reached 50%.[7]

The wealth bonanza created through tech innovation should be celebrated. The founders and key employees of the Cerberus companies captured only a fraction of the value they created; they have multiplied their passive shareholders’ wealth many times over.

But success always breeds envy. Especially when others’ success feels close and visible, as in our self-promotional digital world. Keeping up with the Joneses becomes more expensive when Instagram, LinkedIn and other social networks curate a hyper-targeted set of social reference points for each of us.

The pattern of envy is as fractal as the superstar effect. It does not manifest itself as peasants showing up at the manor with pitchforks. Low-income counties would not have powered Donald Trump to the White House twice if that were the case. Envy does not play out across the population, but within little slivers of the income distribution, micro personal networks, and ZIP codes.

There is no small irony here. Nvidia – the ultimate winner-take-all, the world’s most valuable company today, and a quintessential immigrant-founder American success story – takes its name from the Latin word for envy (Invidia). Nvidia started out as a video game graphics company, making video games look more lifelike. Its chips now power short form video content on social media. Nvidia powers the modern IT economy’s porting of real life into and back from digital life, which runs on consumer aspiration.

Nvidia’s logo is a green eye – the color of envy. It’s a fitting symbol for the dark side of digital media. Anyone who has spent time on Instagram or LinkedIn knows online life is aspirational by design. Aspiration is a healthy and fertile attribute for the economy and society. It has been core to the American project from the start. But it withers when it is decoupled from hard work. And it devolves into envy if it is strictly appealed to as a ploy to fund more consumption.

[The Agency Paradox: From convenience to passivity]

“We intend to build the world’s most customer-centric company. I constantly remind our employees to be afraid, to wake up every morning terrified.” ~ Jeff Bezos, 1998 Amazon Shareholder Letter

“People with very high expectations have very low resilience... Unfortunately, resilience matters in success. I don't know how to teach it to you except for I hope suffering happens to you.” ~ Jensen Huang, 2024 Stanford University speech

Tech’s final dominant first order benefit has been convenience. Once you know what you want, buying stuff has never been easier. This is true across all consumer categories except those that have been sheltered from tech’s creative destruction (like health care). We should all be grateful for it. Compare how much easier it is to quickly get to what you want buying a niche household product on Amazon or renting a place on Airbnb than it is to confidently pick the right health insurance plan during your next open enrollment period.

No set of companies has appealed pitched our inner consumers more persuasively on convenience and friction removal than this era’s winning consumer internet companies. As the above quips illustrate, convenience is delivered to the many through the pain and paranoia of the few.

This is the defining paradox of this era’s tech ethos. The channeling of individual pain and suffering into new invention has broadly delivered convenience and comfort – but also eroded our collective capacity for suffering as these comforts scaled to everyone and became ambient. Too often the profits on “high agency innovation” inside the consumer internet have by earned through millions of users slowly and unconsciously relinquishing their agency.

Most internet companies follow Amazon’s relentless focus on “customer-centricity” and removing “pain points.” As the consumer experience improves, expectations rise – pushing tech innovators into continuous improvement cycles.[8] This cycle of product improvement predates the internet. It played out for cars, dishwashers, etc. But the internet intensified it, collapsed the cycle time, and did so from a starting point of much higher comfort. As expectations rise, consumers’ collective resilience falls.

Personal agency withers without resilience. And resilience is just as critical an ingredient for success as aspiration is. To fund consumption, all of us except those living off inheritance or welfare must be producers in some capacity. Too much convenience silently and insidiously robs us of opportunities to step up and contribute in small but important ways to others in our tribes and communities.

The perverse irony: this “pain-to-convenience flywheel” that makes day-to-day life easier also makes the consumer base less resilient. It erodes our industriousness, persistence, and capacity for creation. The benefits to our inner consumers come at the expense of our inner workers.

The behavior changes that technology companies deliver at scale dilute to the work culture that is required to produce them. A 2022 study from the National Foundation for American Policy concluded that 55% of U.S. tech unicorns (e.g., startups achieving a $1B+ valuation) have at least one immigrant founder. 64% have at least one immigrant founder or first generation American.[9] This compares to base rates in the U.S. population of 16% (immigrants) and 28% (immigrants plus first-generation Americans).[10] No wonder.

Part 5: Winning In The Shadow of The Cerberus

Think about Amazon, Bezos, customer-centricity and a tight deadline for shipping new products. When it all work out, who really wins? The driven Amazon employee whose fledgling product scales and who gets to share in the financial upside? Or the product’s eventual super users?

The question poses a false dichotomy. Maybe you think both win unconditionally. Or maybe you think neither does. But force yourself to choose between the personas. If I had to choose, I’d rather be the tech worker.

The driven worker and the super user may both be stressed and time-strapped. Both likely have disposable income. They may even be the same person: the tech product manager who goes home after a fourteen-hour day to a Netflix show, a DoorDash burrito, and an Amazon prime box on his doorstep.

Tech executives refer to these super users as “high lifetime value” (LTV) because they wind up spending the most money and return to the products most frequently. Said another way – they offload more of life’s daily chores to software. Some do it to free up time to work more. Some may even do it to spend more time with their loved ones. But honestly – a lot do it just out of laziness. Or boredom.

The tech worker is much less likely to be bored than other super users. Most importantly, he gets paid if his creation works out. The fruits of his labor give him options for what to do with the next chapter of his life. The lazy user? He becomes the profit center. Or, in the case of ad-based models, the product itself.

When we think across economic personas, it becomes clearer that the best products are somehow flytraps. Shaping the game as a worker delivers a more enduring abundance dividend than just passive consumption of the product itself.

[1] Apple smashed this target, selling 13-14M phone units in 2008. As of late 2025, Apple has sold more than 3 billion iPhones since inception (publicly confirmed by CEO Tim Cook on the Q3 2025 earnings call).

[2] AWS was not the world’s first cloud computing venture. Many credit that to LoudCloud – a late 1990s start-up founded by Marc Andreesen and Ben Horowitz of Netscape (and later founders of a16z, one of the top five largest venture capital funds globally by AUM as of early 2026). LoudCloud offered managed IT infrastructure before the “cloud computing” metaphor emerged. It experienced high growth in the late 1990s but eventually had to pivot to a pure-software business model, as it couldn’t secure the funding needed to build a pure cloud infrastructure business at scale.

[1] Phone Screen Time Addiction & Usage - New Survey Data & Statistics. Based on a Harmony IT survey of 1K+ Americans, where they self-reported screen time stats from their phones – “We had each generation look up their average daily screen time on their phone and share the numbers.” Studies from 2011 (Recode) put daily mobile phone screen time at 45 minutes in 2011.

[2] Reviews.org survey of 1,001 Americans. (Screen Time and Internet Usage Statistics 2024 | Reviews.org).

[3] U.S. Census Bureau via FRED, series ECOMPCTSA

[4] Rosenfield study.

[5] Based on the author’s analysis of the Forbes 400 list in each year. In each year, I tagged the individuals as “Yes” if a majority of their wealth was earned through founding, building or investing in information / software technology companies and “No” otherwise.

[6] The S&P 500 is a group of the 500 largest publicly traded companies in the U.S. Liquid market capitalization refers to the value of the equity of these companies that is not held by founders/controlling parties. For most companies, the vast majority of equity is liquid – so think of this as a good proxy for the total equity value of the 500 biggest and most important U.S. companies.

[7] This calculation includes in “Technology” companies like Amazon, Tesla, Airbnb, Booking, DoorDash and Uber. The S&P 500 includes these companies outside the XLK technology sub-index, but they are obviously technology companies by a common sense definition.

[8] Don’t be fooled by caricature portrayals like The Internship movie. There is a cushy side to tech-corporatism, but the workers driving the real disruptive innovation are grinding furiously. This dichotomy is explored in Book One, Chapter Two.

[9] National Foundation for American Policy (NFAP) report (data as of May 2022). https://nfap.com/wp-content/uploads/2022/07/2022-BILLION-DOLLAR-STARTUPS.NFAP-Policy-Brief.2022.pdfhttps://nfap.com/wp-content/uploads/2022/07/Immigrant-Entrepreneurs-and-Billion-Dollar-Companies.DAY-OF-RELEASE.2022.pdf

[10] (Key findings about U.S. immigrants | Pew Research Center).

Member discussion