Building The Book

Summary: This is the third sister essay to “The Game of Capitalism” and “Beyond The Game.”

“The Game of Capitalism” offers an insider’s descriptive summary of how modern capitalism works and a framework for understanding how game strategies interact across our different economic personas – owner/shareholder, worker, consumer, and taxpayer. It closes with the argument that The Game needs non-economic values – selflessness, trust, dignity – that it cannot engender or sustain by its own logic.

“Beyond The Game” explores the complex dialectic between The Game and the foundational values it runs on: how The Game can undermine its foundation through its own decentralized competitive adaptation process.

Part One of this essay evaluates our invisible economic persona: the shareholder. It argues the case to invest for everyone – not just the entrepreneurs, private business owners, and professional investors who are already thinking hard about their inner shareholder.

The rest of the essay focuses on the process, craft and ethics of investing in the most accessible way possible: buying stocks in publicly listed companies.

Part Two explores the spectrum of investment strategies in public equities. It shows how capital is increasingly flowing to the extreme ends of the strategy continuum: purely passive indexing and high velocity active trading. Each of these strategies represents its own strand of nihilism regarding the ostensible purpose of investing (e.g., allocating capital). The Game’s own competitive adaptation has resulted in an industry landscape that is increasingly divorced from its ostensible social function – directing capital towards its most efficient use in the real economy. The ideal investment approach will vary across individuals. I argue that for most, a combination of passive indexing and direct stock picking personally is the right one.

Part Three is about how to make money picking stocks. It argues that there are only two ways to increase your return beyond what you get in a passive index strategy: by finding secrets and trading rumors. There are countless secrets and rumors to be discovered. And almost as many strategies to go find them. The key is to find an approach that fits your personality and plays to your strengths. I offer my own approach that I have developed in my years as a professional.

Part Four closes by evaluating the relationship between ethics and investing. I make the case against taking a crusader’s ethical certainty into investing, for two reasons. First, because The Game of Capitalism is too dynamic to have perfect foresight into the ethical implications of a company’s strategy. Assuming such foresight is a form of epistemic arrogance. Second, and more practically, because your gradient of real-world influence per dollar of capital that you allocate will be very low as a small-scale investor. If you want to change the world – go find something else to do. Investing well will earn you money. It will teach you to be a sharper and more dangerous thinker. But your ceiling for real world impact through this domain is vanishingly low in all but the most extreme career outcomes.

In some sense this makes the game of investing a selfish pursuit – unless you eventually port the learnings into other life domains where you can actually move something. Investing offers you the lessons and secrets to bend The Game of Capitalism towards your vision of a good life. But not the platform to do it.

Readers who are professional investors or are otherwise already putting their own money to work in the stock market will be fully familiar with the Parts One and Two. Feel free to skim or skip. Parts Three and Four are for everyone.

Part 1: Why Invest – Money Is Time

You could fill an entire bookshelf with pop investment philosophy books aimed at motivating individual investors. Most contain valuable truths and there is no need to rehash them all here. A Little Book of Common Sense Investing (2007) by Jack Bogle, One Up on Wall Street (1989) by Peter Lynch and The Psychology of Money (2020) by Morgan Housel are three of my favorites. Bogle’s book convincingly argues why the average investor should just own the market cheaply and hold it forever. Lynch’s book offers a fun and exciting counterpoint – that most of us can find a sleeve of companies or pocket of the economy where we can have “edge” and outperform the pros at stock picking. Housel’s book elegantly frames the project of investing against the life’s broader behavioral and psychological elements that can derail the best laid plans – even for a smart and committed investor. The truths in all three books have aged well. They are still worth reading today if you have not already.

There are two more truths worth covering beyond those detailed in the existing canon.

First: investing is the highest leverage activity we can pursue to accumulate the game’s most valuable assets: time and self-awareness.

Second: active investing is probably the best education one can buy in how The Game of Capitalism actually works. I guarantee that having an informed inner shareholder will improve the decisions of your inner consumer, worker and taxpayer. Only a little at first. But the information will compound.

Regarding the first truth – the direct output of The Game of Capitalism is wealth. That’s what companies and business owners are trying to compound. Wealth buys you stuff. But the truth is that stuff is not The Game’s most valuable resource: time and self-awareness are. Paradoxically, the game increasingly calls upon these resources – your time, attention, and desires – as inputs into its own wealth compounding process. The truth is not even a secret – it’s hiding in the “time is money” cliché you've heard a thousand times and probably still ignore.

The secret that investing teaches is to invert the cliché – to think of money as time.

Traditional finance theory teaches the “time value of money” – that a dollar today is worth more than a dollar tomorrow. Inflation and uncertainty erode the value of your money today. The implication is that you might as well do something with it today (e.g., spend it).

This is first order true and probably the right framework for cash-rich companies, families and individuals. But it is somehow exactly the wrong life takeaway for most people – especially the young.

If you can avoid mistakes in investing, your cash today becomes a strategic asset that compounds silently while you actively play The Game. More money is the secret weapon that takes the pressure off time as The Game’s most valuable resource. If time is money – and it is – and you already have plenty of money, you can afford to “waste” time. Sure, money can buy you more stuff – but its real value lies in the degrees of freedom that it buys you over how you spend your time.

This framing makes your inner shareholder your highest leverage persona in The Game. He kills two birds with one stone. When he does his job right, he protects you from wasting your money on frivolous consumption and silently earns you money beyond your day job.

If you can remove the constraints that a lack of money places on your time and that consumerism places on your imagination — the game board suddenly opens up massively for you. You will see a lot more ways to win. Your inner shareholder is the persona that can move you from getting played to playing The Game.

Your inner shareholder can either this leverage for free by investing in index funds (more on that below), or he can sweat for it a little. He can pick some stocks to own.

The latter route requires curiosity, thinking, some pain tolerance, and an appetite for risk. But pursuing it has a second-order benefit: it is a real world, skin-in-the-game education in how capitalism works. This education promises the lesson of the self-awareness that only losing can teach. There are no 4.0 GPA investors. You will lose on some ideas.

The knowledge and lessons that active investing throws off can compound like money. They can open up hidden opportunities in your life that you never would have spotted otherwise.

The next section explores how to think about the tradeoffs to your inner shareholder between opting for purely passive leverage or putting in the sweat to try to pick some of his own leverage points.

Part 2: How To Invest – The Sound & Fury of Public Markets

Ask a professional investor what the point of their job is and you will hear one of two answers. The obvious answer is a version of: to make as much money as possible, within the rules of the game. The second potential answer is something like: “the point of my job is price discovery – pushing the prices of assets to their true value. This helps everybody because it pushes capital to its best uses across the economy.” This second point is technically true. Collectively, investors are the guardians of The Game at the highest level. For most of capitalism’s history, this has made investing deeply important and even noble work.

The paradoxical reality is that competitive adaptation has caused capital to flow to the extreme poles of the strategy landscape where the price discovery function – the one that justifies the investment management industry’s existence – is essentially abdicated. Both of the winning strategies of the past decade (passive indexing on one end and manic pod shop trading on the other) are sullied by an uncomfortable nihilism: the business models are entirely divorced from the only purpose of the job beyond making money.

Let’s take their nihilism in turn.

With all their buying and selling, active investors ensure the market is reasonably efficient. That makes it possible for the rest of us to do the sensible thing, which is to index. Want to join me in this parasitic behavior? ~ Paul Samuelson

The passive investor has made peace with a straightforward bargain: he will accept whatever price the market sets, contribute nothing to the process of setting it, and collect his proportional share of whatever The Game produces. It is the financial equivalent of showing up to a potluck and eating everything on the table. Indexers are freeloaders.

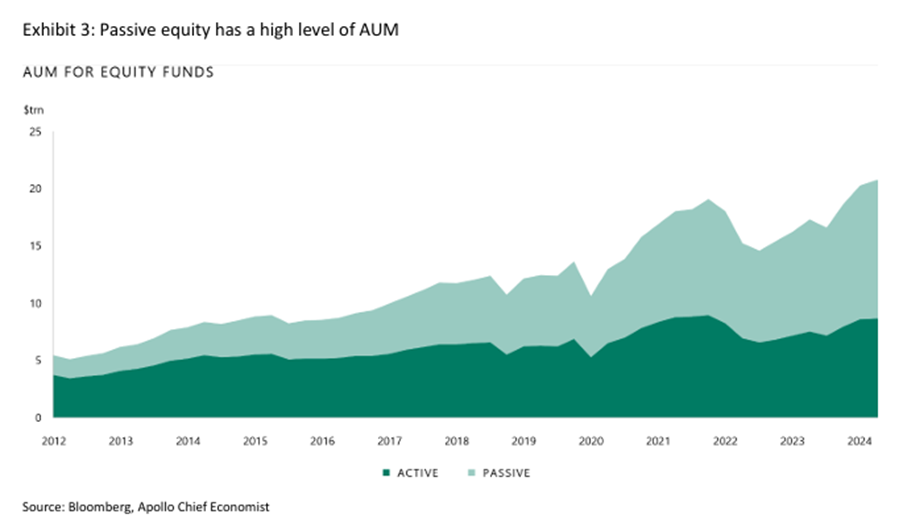

Increasingly investors are on Samuelson’s side – they are OK with being nihilistic parasites. The above chart from Apollo Academy shows that passive investment strategies have taken more than 80% share of the incremental dollars managed in public equity strategies in the last 10-15 years.[1]

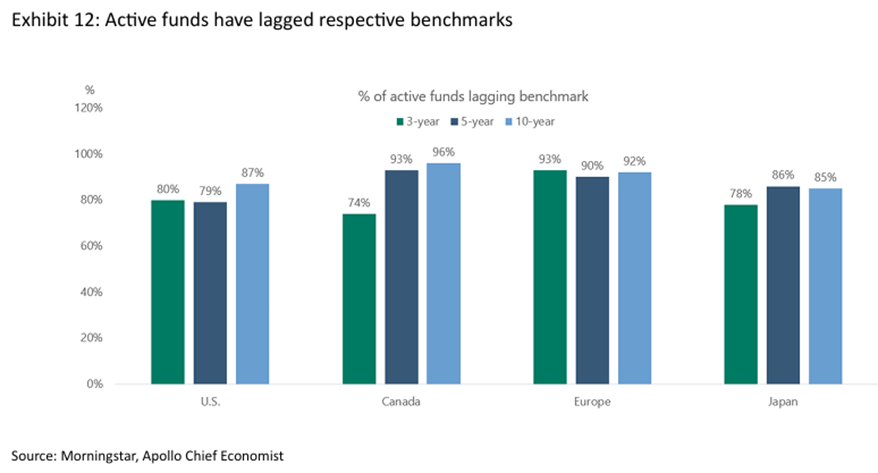

Most indexers (me included) are not proud to abdicate the noble responsibility of price discovery. We do it because it makes financial sense. Most active management strategies are bad products for the clients: ~80-90% of professional active managers cost their clients’ money over the medium and long term. They deliver worse returns than the passive indexing strategy that their funds’ returns are benchmarked against. It is hard to get moralistic about financial services customers’ long, slow drift towards free-rider nihilism when you look at the alternative product set.

Further, while price discovery sounds noble we should not reflexively celebrate a high number of people engaged in it. Feeding people is noble too – but you don’t hear many people mourning the decline of farming as a profession as agricultural technology got better. Indexing strategies are arguably just technology that automates a real human need for price setting. Anyone who totally rejects passive equities as a beachhead allocation in their investing strategy is either a very special talent, or crazy. Maybe both.

At the other end of the strategy spectrum from passive indexing is the high volume trader – epitomized by a portfolio manager at a market neutral platform fund (or pod shop). His nihilism is less obvious but more complete. His holding period – often measured in days, sometimes months – is a structural confession that he has no real conviction in what a business is worth or how it is evolving. His dollar of capital deployed reflects virtually nothing of his belief about how the company he owns will deploy capital, or whether the business activity that emerges downstream of that investment is efficient or good. He is just renting probability asymmetries around near-term catalysts and then moving on. The company is only the occasion for the trade.

This business model is more of a poker game than a price setting mechanism. Forget price setting – the manic trades and the financial leverage underpinning them occasionally introduce more short-term price noise than signal. High trading volumes speak a dangerous world that runs on sound and fury, not quiet clarity.

Life’s but a walking shadow, a poor player

That struts and frets his hour upon the stage

And then is heard no more. It is a tale

Told by an idiot, full of sound and fury

Signifying nothing

~ William Shakespeare, Macbeth

Macbeth was a mercenary making a power play. He took his shot at the crown, became king, got found out, and then got murdered. The career arc of many hedge funds pros – especially those at market neutral platform shops – is not so different. Median portfolio manager tenure at the largest platforms runs between two and three years; for analysts it is even shorter. The platforms are designed as elimination tournaments, not careers. Most players get cut.

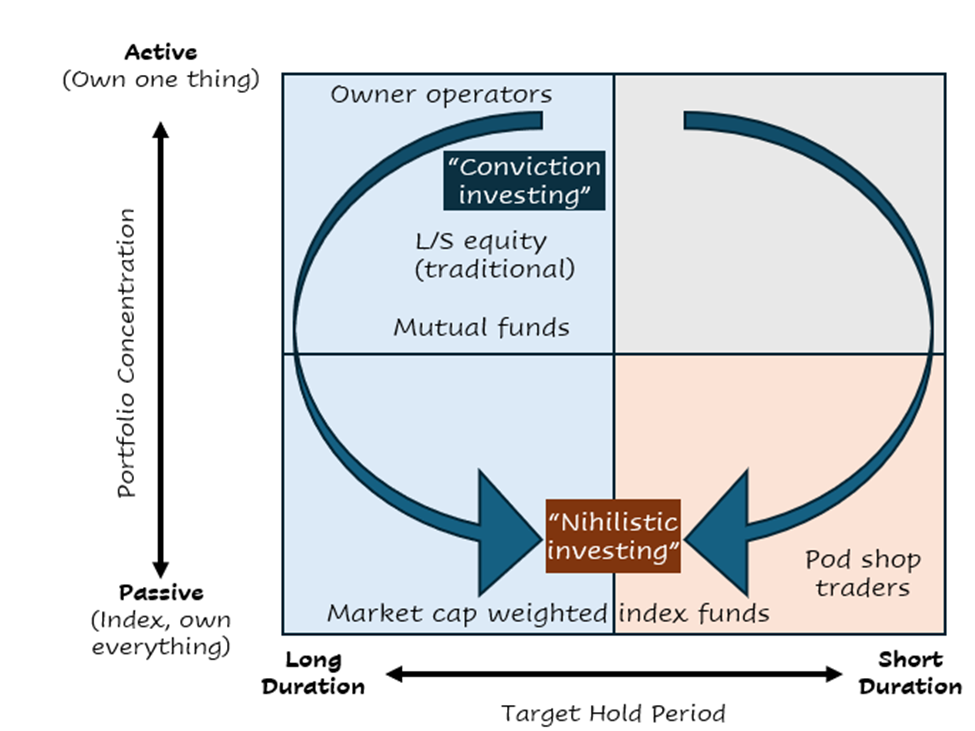

Thirty years ago, index investing was a niche strategy within the money management business. The industry was dominated by mutual funds charging 1% management fees to invest in a smaller portfolio of stocks (50 – 100 companies typically). The hedge fund industry was still nascent. The business models of equity long/short hedge funds arguably looked more similar to traditional mutual funds than to the market neutral platform hedge funds of today.

Both mutual funds and traditional long / short equity hedge funds had business models rooted much more cleanly in price discovery. Julian Robertson, probably the most famous hedge fund investor of the 1990s, described his mandate as “to find the 200 best companies in the world and invest in them and find the 200 worst companies in the world and go short on them. If the 200 best don’t do better than the 200 worst, we should probably be in another business.”

Industry assets under management didn’t drift away from these traditional strategies focused on price discovery because clients stopped believing in it. They drifted because these strategies produced return streams that started looking too much like those produced by low-cost indices, and were deemed too expensive. Why pay 1-2% for what you can get for 0.1%? Most clients eventually stopped.

The capital that remained in active management migrated toward the one thing active strategies could still offer that indexing couldn't: uncorrelated returns. A strategy that produces a return stream that matches the S&P 500 but delivers positive results when the stock market index is down is an extremely valuable form of insurance to some investors. This is what the pod shop model promises and what the best pod shops deliver. That’s the answer to competitive adaptation that The Game produced. Not price discovery – but a sophisticated bet on other people's price discovery. Often at 30 days or less per position.

This industry structure evolution points to an existential conclusion for individual investors: that there is nothing left for most of us to do. The Game has increasingly competed out professional active managers. The pros that remain increasingly work in pod shops where tight risk control systems drive most of the outperformance for the client, not the specific portfolio managers. Human judgment looks less relevant than ever in the business of public market investing.

The natural reaction to this industry evolution is concession: to simply embrace the nihilism. Put everything in the lowest cost index fund and clip an indiscriminate coupon on The Game of Capitalism. If you're wealthy enough, maybe add a market neutral fund for uncorrelated insurance. Outsource everything. Abdicate judgment.

Empirically this looks rational. For most of your money, it probably is. The data on active management is damning. Why pretend otherwise?

But a full embrace of the concession strategy treats your inner shareholder as a passive recipient of whatever the market produces – not as an agent with the capacity to know things, find things, and build conviction in ideas that other people haven't seen yet. The concession strategy may be financially defensible, but it is epistemically self-defeating. It is applied determinism – a tacit admission to having no original insight to how The Game of Capitalism is played (at least by the big public companies). And having nothing to contribute to the process of understanding what businesses are worth.

I categorically reject such a defeatist admission for myself – and for any intelligent, curious person that is willing to do the work. I’d rather lose a little performance relative to the market than wholly accept the irrelevance of my own mind.

Professionally managed capital went to the strategic poles. But there are still profitable ideas to find in the vast middle between indexing and leveraged short duration bets. The trick is to ask yourself which ideas you are uniquely suited to chase. The answer to this question informs when and where your inner shareholder has the right to leave the bench of parasitic indexing and jump in The Game.

Part 3: The Craft of Alpha Generation – Rumors & Secrets

The list of disadvantages you have relative to a pro investor is long. The pros work on their portfolio full time (often with analysts underneath them), get to meet with company management in between quarterly earnings calls, and have the scale to pay for research and data resources that you do not see. But for every advantage, there is a hidden list of structural advantages on your side of the ledger.

First – if you are keeping the vast majority of your equity investments in low cost indices, you should not have to worry about diversification. If 90%+ of your equity portfolio is in indices – that is your diversification. You can choose to put your active money in one or two ideas if you want. A pro could never do that.

Second – if you manage your household expenses with enough cushion, you should not have to worry as much about drawdowns. It may be painful to watch the prices of stocks you own drop, but it’s nothing compared to the pressure of having to report the numbers to clients in a down month and write a letter explaining why you are not an idiot.

Third – because you are small trader, you will almost never be a price setter in the market. When you are wrong on an idea, you can almost always get out of it quickly without dragging the price lower. The pros have to worry about liquidity; you don’t.

Finally – you don’t have to argue with other people on your team about which ideas are the best. Productive debate within a high trust team is an asset. But passive aggressive back-and-forth between analysts and portfolio managers that do not like or trust each other becomes a liability that compounds over time. Bad blood distorts judgement. There is far more bad blood in the industry than the marketing dossiers and sycophantic podcast interviews would have you let on.

The final trick is to figure out where to put these advantages to work: where you have the right to hunt for ideas and what kind of ideas you are best suited to hunt. This demands probing not only your knowledge base but also your psychological makeup. Before you hunt, know yourself. Are you wired for patience or for action? Can you stomach being early to an idea — watching it lose money before it works? Do you like betting against consensus or running with it? You may not know the answers until you jump in. But ask the questions early and revisit them often.

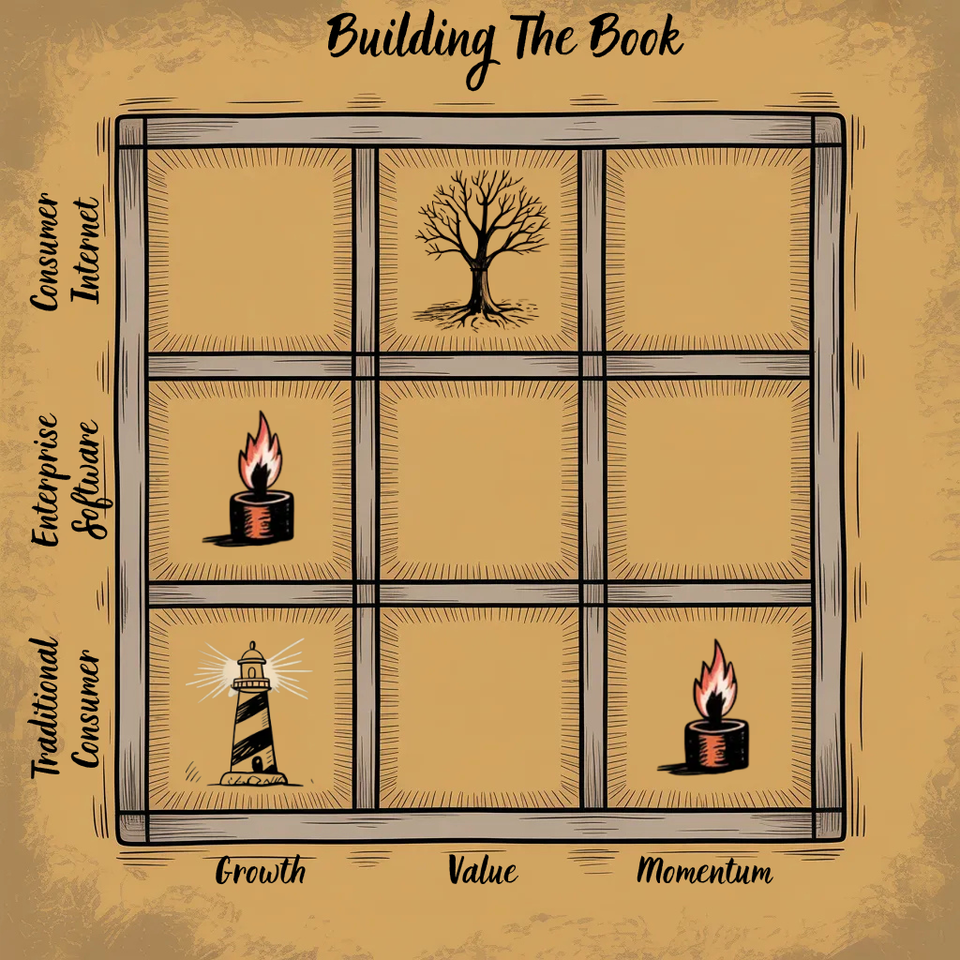

In my own idea generation process, I map the companies I know along two dimensions – first by industry ecosystem and second by “stock characteristic” or factor.[1] I then look at the companies try to ask myself: what is the archetype of this idea? I have three mental archetypes.

1. Lighthouses: The largest and most important companies in their ecosystems.[2]

· These are the companies that the smaller ones revolve around and react to. They are lighthouses not just because they are big and important, but because they shed light on everything in their vicinity.

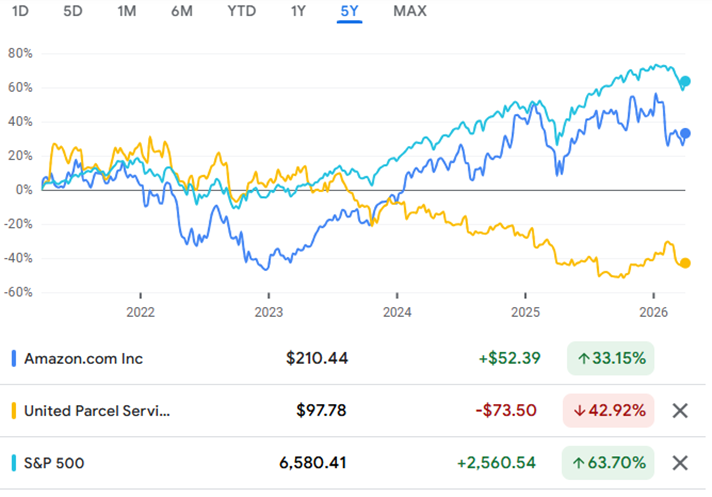

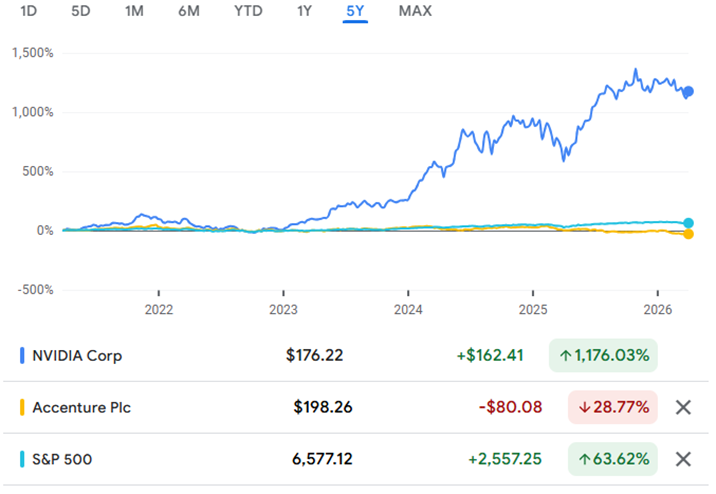

· They change how you see companies that surround and compete with them. Consider the relationships between Amazon and UPS. Or Nvidia and Accenture.

o What you needed to short UPS coming out of the COVID pandemic was (i) knowledge that Amazon was its biggest customer and (ii) conviction that Amazon had overbuilt its own distribution network during COVID. The natural strategy pivot for Amazon to correct its overbuilding mistake would be to in-source more of its shipping volumes to drive up utilization rates. The natural loser of that pivot was its biggest outsourced partner – UPS. Not everyone covering UPS was thinking hard about Amazon’s fulfillment network.

o What you needed to short Accenture from the “ChatGPT moment” in November 2022 was the knowledge of AI scaling laws and their implications for demand for Nvidia’s products. Accenture sells human coders for hire – Nvidia’s customers were building the technology for code to write itself. Before ChatGPT, few thought Nvidia’s business model was a relevant leading indicator for Accenture’s demand. Now – it is arguably the main governor of Accenture’s stock price.

2. Trees: Companies that have strong foundations and can grow (compound) for years. They are often challenger companies on a slow march towards lighthouse status.

· Trees are rare because the competition of capitalism is intense.

· They make for the best investments when you identify them early. They are fine-to-good investments when you identify them on time. They prove disastrous investments when you find them late (and the rot is setting in). The trick with trees is knowing which phase you are in.

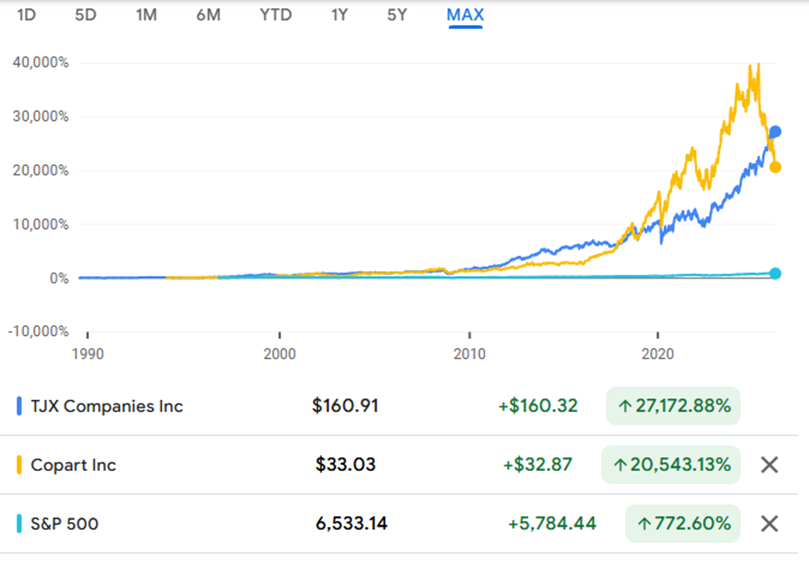

· Compare TJX (the off price clothing retailer) and Copart (the car auction salvage yard operator). Both have been amazing trees since IPO. If you just had a little patience, there have been almost no periods when your future self would not have been happy that you bought TJX. You could have said the same about Copart – until a year ago. In the past year its stock is down ~40% against the S&P 500 up ~15%. Copart is still a great business. But is rot setting in? You have to know if you want to own it today. Owning Copart today would demand much more of you than owning TJX.

3. Trades: Everything else – and 90% of public companies out there.

· These companies have good quarters, then bad ones. Good years followed by bad ones. Then they eventually die.

o Their fortunes are usually more dictated by the macroeconomic and industry conditions than their own strategies.

o When their strategies do find momentum, it’s often hard to sustain for more than a year or two.

· The academic Hendrik Bessembinder quantified why this taxonomy matters. The top 4% of listed companies account for the entire net gain in the U.S. stock market since 1926. Lighthouses and Trees live in that 4%. The other 96% did no better than cash. If you are forming an idea within the 96% - you need a strategy and a plan for when to get out.

· When you zoom out, their stock charts often look like jagged lines to nowhere – usually on the way to some still unforeseen, unceremonious end. They are like Macbeth: poor players strutting and fretting their hour upon the stage, until heard of no more.

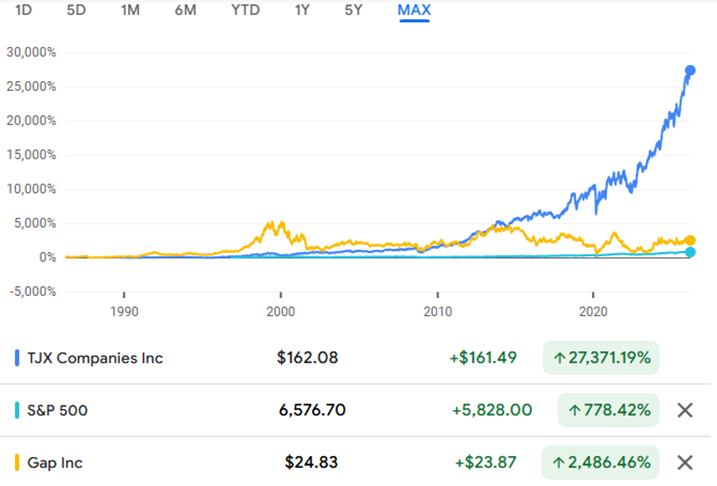

o Consider the case of TJX against The Gap. The Gap outperformed the market (and TJX) in the late 1990s when it dominated the cultural zeitgeist. But the stock is down 45% in the 21st century. Out like a brief candle.

From this mental map, there are only two ways to consistently out-earn the passive index funds that should anchor your portfolio: invest in secrets or trade rumors.

I borrow this concept of secrets from Peter Thiel. He asks in job interviews: What very important truth do very few people agree with you on?[1] If you have a good answer, that is your secret.

Investing in secrets is about getting in and out of the lighthouses and trees at the right moments in their company evolution. If you own the big indices, chances are you already own most of lighthouses and the trees. Owning the index means that you own almost all of the big winners – but also some still great companies that are past peak. This latter category tend to be terrible stocks. If you own the S&P 500, you own TJX and Amazon. But you also continued to own UPS as it was over-earning coming out of the pandemic. And Accenture as the existential AI risk metastasizes and threatens its core business model. And Copart as its top competitor gets its act together after years of serial mismanagement. Etc.

The advantage you bring is knowing which trees/lighthouses to size up and size down. To do that, you need to believe you are right about some enduring secret that most people have not woken up to yet.

Trading rumors is about being early to and right on new stories on littler, less consequential companies. You can get paid even if your little story never becomes big, even if your trade never grows into a tree. Maybe your story is only a rumor; maybe it isn’t. Maybe it turns out to be consequential, but probably not.

The point is that it does not matter: the stock market is full of flighty, manic hands. So rumors will move the market – that creates opportunities to make or lose money.

But beware – trading rumors us doubly hard. Not only do you need to know when you have a story / rumor that will move the price, you also have to know when its going to become irrelevant and get out before it does. The price moves driven by rumors are much more ephemeral than the unfurling of big secrets of trees and lighthouses.

A further note of caution – there is an enormous temptation to imagine that your rumor is actually a secret – especially when it is making you money. And especially if (like me) you are wired to be a secret hunter. It is deeply flattering to believe that you have uncovered some big thing that no one else knows yet. Without great discipline, this is how you will interpret the price of a “rumor idea” going up and making you money. But you need to remember the historical base rates that Bessembinder established: 95%+ of stocks do no better than cash in the long run. It always feels wistful and unsatisfying to sell a winner. And it hurts to sell early. But it hurts even more to hold on too long. And the rules of The Game of Capitalism bias towards the second outcome as more likely – especially if you are riding big gains on a mediocre company.

So it’s best to assume that every non-obvious idea is a trade. Trades can be measured in weeks, months, quarters. Maybe a couple of years – but no more. Big secrets unfurl in years.

You need to go into a trade with a plan for when (or what price) you will exit the trade if it works, and stick to the plan. This is a much harder problem for professionals than for you. If a professional cashes out on a trade, he will feel pressure to know what idea to recycle that capital into. If you don’t have a good idea – you can reinvest your profits back into your parasitic index fund and no one will think worse of you for it. Trades are where your duration, concentration and liquidity advantages play strongest in your favor too. I try not to get too promiscuous with trades; I know I’ll be wrong a lot. I always think poorly of my past self for going after a frivolous idea if it starts losing money. But years of experience has given me some pattern recognition for what makes for a decent trading setup.

The hardest thing about investing is not generating interesting theses. It’s categorizing the theses and then building an action plan to monetize them. Is this true? Is it a secret? Will it matter more tomorrow than today? Is it a big deal?

A big truth that is not a secret is typically (but not always) reflected in the stock price and earnings expectations for a company. A truth that is not known is not necessarily a secret – it may just be an ephemeral rumor. And a rumor doesn’t even have to be true to move the stock price – it just needs to be something people focus on more tomorrow than today.

When I stitch together an investment thesis, I try to pressure test it against the four above questions. The first two are more analytical – you can usually work them out in your head with enough research and rigor. The second two are more instinctual. They have to withstand scrutiny of the heart and gut. Markets are made of people, and people move on feeling as much as fact. Conviction is a test of the heart: do you believe the thesis is important enough to fortify your belief in an inevitable stretch when the market disagrees with you? Timing is a gut check: are you near the moment when secret starts getting out – when the gap between what you know and what the market prices begins to close? You can be completely right about the secret and still lose money if your gut is wrong on the timing and your heart lacks the conviction to stick it out.

If you have confident yeses to all four questions, your idea deserves a real position. If you can’t get to confidence on any of them – especially the first two – don’t bother with the idea. If you have confident yesses to a couple of the questions, start small and use your judgment as you try to sort out the answers to the remaining questions. Clarity is more likely to come with a little pocket change on the line.

Part 4: Ethics & Investing – The Loose Garment

The sister essay to this one — Beyond The Game — maps the complex dialectic between the pursuit of wealth and the ethical foundations that sustain it. That essay works at the level of society and culture. This section brings the same dialectic down to the most personal and practical level: what should guide the ethics of an individual's capital allocation decisions.

The core idea is that ethical considerations should fit over a portfolio of actively managed public equity investments like a loose garment – not a straitjacket. This seems counterintuitive from the claims of the other two essays. The Game of Capitalism establishes shareholders as The Game’s most powerful players. Beyond The Game documents the damage inflicted when The Game encroaches on the ethical foundations that should underpin it. The shareholders are the guardians of The Game. Should they not be the first line of defense against corrosive encroachment? The first order logic is seductive. But it turns out not to work so well.

The first failure point of this “investor as ethicist” logic is it misunderstands the adaptation patterns of capitalism. The Game is governed by unpredictable creative destruction. Consumers’ preferences and companies’ strategies evolve in ways that are hard to anticipate. If you do not have perfect foresight into how The Game will evolve – and you don’t – you can’t build a portfolio that reflects a coherent ethical worldview through time.

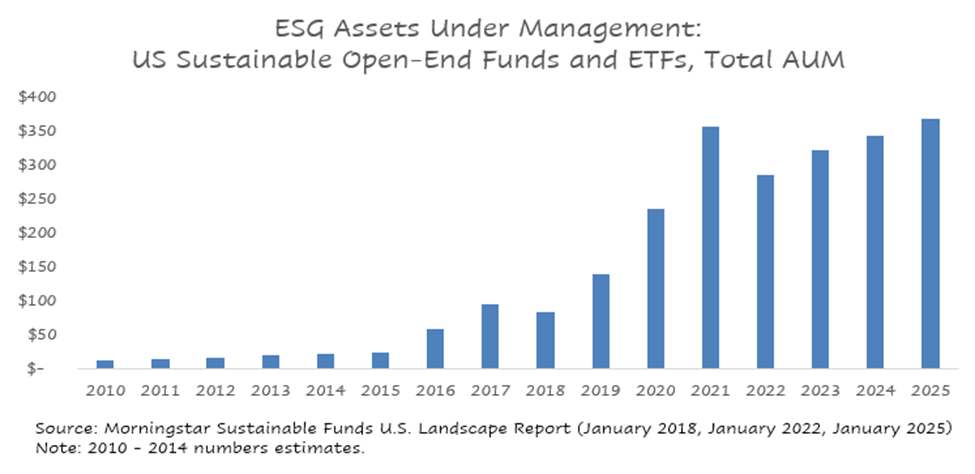

Consider the conceit of the Environmental, Sustainability, and Governance (“ESG”) movement. ESG strategies gained considerable assets under management (“AUM”) coming out of the financial crisis of 2008 – 2009 until their inflows peaked in 2021. The ESG movement gained influence in the shareholder zeitgeist largely by criticizing energy companies like ExxonMobil, Shell and BP. At the dawn of the ESG heyday these companies comprised a larger portion of the S&P 500 index than they do today. By refusing to own them, ESG strategies were effectively overweight Big Tech through the last 15-20 years – and they outperformed because they owned Big Tech. In the past decade ethical critiques of The Game have shifted to focus relatively more on the attention economy and the extractive nature of digital business models and relatively less on fossil fuels. The ESG funds effectively grew assets by being overweight the future “ethically dubious businesses” exactly while these businesses were scaling and diffusing through society. The ESG movement peaked in late 2022 when the energy stocks they refused to own began to dramatically outperform the broader market for the first time in decades and as Big Tech temporarily underperformed. A strategy that looked for years like “doing well by doing good” was exposed as an incoherent, self-regarding, and self-enriching form of epistemic arrogance.

The paradoxical reality of public markets is that the legion of shareholders that own the companies are simultaneously The Game’s most powerful players and its most ineffectual. Shareholders of successful companies get rewarded handsomely for picking them. But they rarely contribute much to defining the companies’ cultures and strategies or executing successfully.[1] When shareholders do actively contribute to a company’s success, it is usually through removing some bad ingredients – getting unproductive workers fired, or cutting down wasteful investments – not through adding positive ones. It is hard for shareholder ethics movements like ESG to deliver against their goals precisely because a company’s ethical impact is too finely woven into its strategy and execution detail to be altered by a distant and anonymous shareholder base. The shareholder base cannot reach down into the level of reality where the ethical impacts manifest.

If your dollar of invested capital allocated has a de minimis impact on the future strategy and execution of the company, does it bear any ethical load? From a first principles sense, always. But practically? Not really.

In my own portfolio, I’m a pragmatist about this stuff – not an absolutist. I weigh decisions of which companies to own against both the “degree of real-world influence” of my invested capital and the ethics of the company’s strategy/mission – and make judgement calls. For instance, I’d never invest in OnlyFans or cannabis companies under any ownership structure – they are too toxic to society. And I would never have gone to work for DoorDash or become an early private investor – I have no respect for the company’s mission. But what’s done is done: DoorDash forever changed consumer behavior. I’d own the stock for a nice trade if I thought it got cheap enough and the fundamental case was good enough. Let’s not kid ourselves: no one will be damned for overpaying for delivery of too much crappy fast food. And my capital has essentially no influence over that consumer’s behavior.

If this approach sounds compromising, well – investing is hard. Some spheres of life require total conviction in a big vision and the conviction to live by it. Other spheres demand flexibility, curiosity and adaptation. Investing belongs in the latter. It’s not a game for theological hedgehogs who only believe “one big thing” – it’s a game for shrewd foxes who are willing to explore, revise, and even drop convictions as they learn.

Your ethics don’t always lead you to gold. And that is OK – ethics was never meant to be alchemy. Just check that the gold you see in your best ideas isn’t paving someone else’s road to perdition.

Ethical intuition is not a foolproof north star for finding money in markets. But it is not useless either. It takes basic ethical instincts to work out when a company’s growth strategy transitions from burning good fuel to bad fuel. That instinct, combined with a sense of how easily customers can leave, helps to sort out when a good growth story will break.

The Game's Broken Scoreboard explores this framework in depth — the distinction between revenue growth that makes a company stronger and more beloved versus growth that extracts value from customers who are increasingly captive, addicted, or simply unaware of better alternatives. The transition from good fuel to bad is rarely announced. It shows up first in the texture of the business — in rising customer acquisition costs, declining net promoter scores, management pivots away from the core product promise, or a growing dependence on regulatory moats rather than genuine consumer surplus. An investor with a well-calibrated ethical framework will often see this transition earlier than a purely financial analyst will.

There is a difference in investing between observing something and really “getting it” – e.g., knowing it to be true. The difference is conviction. Conviction is what transforms insight into edge. It is main ingredient for making money in active management, it may matter even more than being right. You don’t have to be right all the time (and you won’t be) if you are convicted in your best ideas. Conviction does not always come from having more facts than your counterparties. It can come from being able to articulate and pattern match the facts in ways that others cannot.

It is far harder to get to real conviction in a company’s trajectory without a coherent underlying framework for making sense of The Game and its adaptation patterns. Ethics in investing are one tool to build that coherence. Without conviction you’ll be far more likely to let stock price action drive your confidence and portfolio position sizes – which, coincidentally, is the exact portfolio construction mechanism of the market-cap weighted S&P 500 index. Ethical instincts, if you have any, can be a tool to build the thing that your passive investment approach nihilistically abdicates. Just don’t convince yourself that ethics is your only tool, or you might overuse it.

Few stock pickers reference ethical instincts as a source of edge – or even talk much about ethics at all. Charlie Munger did – and credibly. Bill Ackman and Ray Dalio have tried at times. But ethical grandstanding is mostly left to the big, faceless firms sucking up passive AUM in indexing strategies (BlackRock). It is hard to tell whether the investor class’s public silence on ethics is attributable to a lack of time, a lack of ideas, or just a strategic moral thinness to avoid dealing with hard questions in public. I suspect that all three factors contribute and even reinforce one another.

Regardless, few seem surprised or perturbed by investors’ silence when it comes to ethics; few even seem to notice it. This is because shareholders largely operate above the fray of The Game. Collectively they exert real influence on The Game and are the most financially levered to its outcomes. But paradoxically, the individual capital allocation decisions of the vast majority of money managers (professional and retail) have only a loose and low fidelity impact on how the game of capitalism gets played out in the trenches of day-to-day reality.

If you want to bend the shape of The Game, jump down into the fray. And then use your unique insights from the fray to find little secrets in the market – just as Peter Lynch recommended in One Up on Wall Street. The doors between your inner shareholder and all of your other economic personas are two way and always open. You will be richer for it – in more ways than one – if you actually use them.

[1] Founder-led companies are the big exception here. Founders are often still big shareholders and lead the companies forcefully. Investors often like to see high insider ownership at companies for this reason.

[1] https://perell.com/essay/peter-thiel/

[1] Factor investing means systematically buying stocks that share a specific measurable trait — such as rapid earnings growth (growth), financial strength and profitability (quality), recent price appreciation (momentum), or low price relative to fundamental measures like earnings or book value (value) — that has historically been associated with above-average returns. You are buying a characteristic rather than a company.

[2] The list of lighthouses changes over time. That’s part of the creative destruction process of capitalism. For context, the S&P 500 is full of lighthouses. Not every company in the index is a lighthouse, and not every lighthouse is in the index. But the main job of the S&P 500 committee is to stay on top of the lighthouse evolution process and reflect it in the composition of the index. Aside from making mechanical changes for merger activities, this is why the committee actively swaps companies in and out of the index a few times a year. One underappreciated reason passive indexing works is that it ensures you are always heavily weighted toward the current lighthouses – the index committee's job is to make sure of it – instead of a bunch of trades that you either get wrong or hang around in for too long.

[1] When you account for asset price appreciation in active strategies, passive strategies are likely taking more than 100 cents on the incremental dollar of invested capital.

Member discussion